Step-by-Step Guide to Towing Reimbursement, Coverage Types & Claim Mistakes to Avoid

Getting your vehicle towed is stressful enough on its own. Discovering afterward that you might have been able to have the cost covered by your insurance but missed the window, used the wrong process, or simply did not know how adds a layer of frustration that is entirely avoidable.

Millions of drivers across the United States pay towing and roadside assistance costs out of pocket every year without realizing their auto insurance policy, roadside membership, or credit card already covers those services.

In Milwaukee, where winter breakdowns, pothole damage, and accident-related towing are exceptionally common, understanding how to file a towing insurance claim is practical knowledge that directly affects your finances every single season.

This guide walks you through everything you need to know: which types of insurance cover towing, what documents to gather before filing, the exact steps of the towing insurance claim process, common mistakes that lead to denied claims, and how to maximize your reimbursement.

Whether your tow was accident-related, a routine breakdown, or a Milwaukee winter recovery, this is the information you need to get paid back correctly.

Related Article: Towing After an Accident in Milwaukee: Insurance, Costs, and Legal Rights

| Disclaimer: This guide provides general information about insurance claim processes for towing services. Insurance policies vary significantly by provider, plan type, and individual circumstances. Always consult your specific policy documents and contact your insurer directly to confirm your coverage details. This is not legal or financial advice. |

Does Insurance Cover Towing? Understanding Your Coverage Options

The answer to whether insurance covers towing depends almost entirely on the type of policy you carry and the specific coverage endorsements you have added. There is no universal answer but there are clear patterns across the most common policy types that every driver should understand before they ever need a tow.

Auto Insurance Towing Coverage by Policy Type

| Coverage Type | Towing Covered? | Conditions |

| Liability only | No | Covers damage to others, not your own vehicle |

| Collision coverage | Yes – after an accident | Subject to deductible; covers tow to repair shop |

| Comprehensive coverage | Yes – non-collision events | Flood, theft, deer strike, fire; subject to deductible |

| Roadside assistance add-on | Yes – broadly | Most common scenario; often no deductible applies |

| Uninsured motorist property | Sometimes | If at-fault driver is uninsured; varies by state |

| AAA membership | Yes | Included by tier; mileage limits apply |

| New vehicle warranty plan | Sometimes | Manufacturer roadside packages vary widely |

| Credit card benefit | Sometimes | Check specific card terms; limits apply |

Roadside Assistance Add-On: The Most Relevant Coverage

For the majority of everyday towing situations breakdowns, flat tires with no spare, dead batteries requiring towing to a shop, the roadside assistance endorsement is the coverage that applies. This is a low-cost optional add-on available from virtually every major auto insurer in Wisconsin, typically priced between $3 and $15 per month per vehicle.

Roadside assistance add-ons generally cover towing up to a specified dollar amount or mileage limit per incident. Common structures include a flat dollar cap per tow (often $50 to $100), unlimited towing to the nearest qualified repair facility, or a mileage cap (such as up to 100 miles). Knowing your specific limit before you need a tow is essential if your tow exceeds the cap, you pay the difference.

Collision Coverage and Towing After an Accident

When your vehicle is towed after a collision, the towing cost is typically covered under your collision coverage as part of the broader claim. The tow is treated as a necessary expense related to the covered loss event.

However, collision coverage is subject to your deductible and if your deductible is $500 or $1,000, a towing bill of $150 to $300 may fall entirely within that deductible, meaning your insurer pays nothing toward the tow itself even though the coverage technically applies.

This is a nuance many drivers discover too late. If the total repair cost exceeds your deductible, the towing cost is rolled into the claim and effectively reimbursed. If the total damage is less than your deductible, you are paying everything out of pocket regardless of coverage.

Emergency Towing Insurance Coverage: What It Actually Pays

Emergency towing insurance coverage through a roadside add-on typically covers the full cost of a standard tow within the policy’s limits. Flatbed tow insurance coverage may be treated the same as standard towing under many policies, but some insurers apply a lower cap to specialty towing services.

Always confirm with your insurer whether flatbed towing, heavy-duty towing, or long-distance towing are covered at the same rate as a standard local tow, or whether separate limits apply.

| Key Insight: Many Milwaukee drivers discover after a breakdown that their roadside assistance coverage was much more generous than they expected or much more limited. The only way to know for certain is to read your policy’s roadside assistance endorsement before you need it. Pull it up today, note your per-incident towing limit, and save your insurer’s roadside claim phone number in your contacts. |

What to Do Before Filing a Towing Insurance Claim?

The steps you take at the scene of the breakdown or accident before any paperwork is filed, have a significant impact on how smoothly your towing insurance claim is processed and whether it is approved in full. Here is exactly what to do in the moment to set your claim up for success.

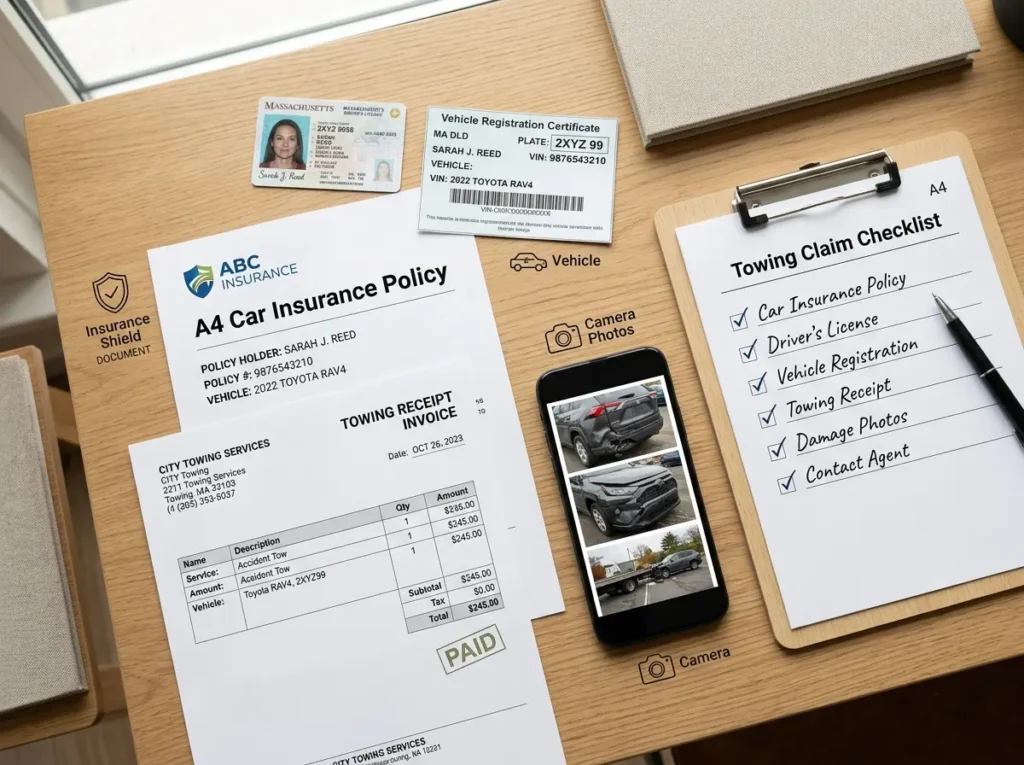

Step 1: Gather Documentation at the Scene

Documentation is the foundation of any successful insurance claim. At the time of the towing event, collect as much of the following as possible:

- Photographs of your vehicle showing its condition before it is loaded onto the tow truck, capture all sides, any damage, and the surrounding environment

- The exact location of the breakdown or accident, note the street address, nearest intersection, or GPS coordinates

- The towing company’s name, license plate number, and operator’s name and ID number

- A written estimate or invoice from the towing company before they begin, this is your right, and a reputable provider will always supply it

- The destination where your vehicle is being taken, name, address, and phone number of the storage facility or repair shop

- Time and date of the tow, confirmed in writing if possible

- If the tow is accident-related: the police report number, the other driver’s insurance information, and contact details for any witnesses

Step 2: Request an Itemized Invoice from the Towing Company

When the tow is complete, request a fully itemized invoice from the towing company before you leave or before you authorize release of the vehicle. The invoice should list every charge separately: the hook-up or base fee, per-mile charges, any after-hours surcharges, special equipment fees, and storage fees if applicable.

Insurance companies are much more likely to process and reimburse claims that are supported by itemized invoices. A lump-sum receipt with no breakdown is harder to process and may trigger a request for additional documentation that delays your reimbursement. Never accept a hand-written total with no line items.

Step 3: Call Your Insurance Company Promptly

Most insurance policies require claims to be reported within a reasonable timeframe of the incident, often 24 to 72 hours for a roadside or towing claim, and sometimes sooner for accident-related claims. Do not wait several days before contacting your insurer.

Call your insurer’s claims line as soon as the immediate situation is under control even if you are still at the roadside. A quick call from the scene establishes the claim, gets you a claim reference number, and may allow your insurer to dispatch their own preferred tow provider at no cost to you, avoiding out-of-pocket payment and later reimbursement entirely.

| Timing Is Critical: Filing a towing reimbursement claim days or weeks after the event is significantly harder than filing promptly. Some insurers have hard deadlines as short as 30 days for submitting roadside assistance receipts for reimbursement. Missing these windows can result in complete denial of an otherwise valid claim. File as soon as the documentation is in hand. |

Documents Needed for a Towing Insurance Claim

Having the right paperwork ready before you call your insurer makes the claim process significantly smoother and faster. Here is a complete checklist of the documents typically required for a towing insurance claim.

Standard Documents for All Towing Claims

- Your auto insurance policy number and the claims phone number

- Driver’s license and vehicle registration

- Itemized towing invoice from the towing company showing all individual charges

- Proof of payment receipt or bank/card statement confirming you paid the tow

- Photographs of the vehicle at the breakdown location before towing

- Date, time, and location of the towing event

- Towing company’s name, address, and contact information

Additional Documents for Accident-Related Towing Claims

- Police report or police report number from the responding officer

- The at-fault driver’s name, insurance company, and policy number (for third-party claims)

- Photos of the accident scene and vehicle damage

- Contact information for any witnesses

- Medical records or injury documentation if applicable even if not directly related to towing, they support the broader accident claim

Additional Documents for Roadside Assistance Reimbursement

- Your roadside assistance membership card or policy endorsement details

- The original service receipt from the roadside provider

- Any pre-authorization reference number given by your insurer’s dispatch if you called them first

| Pro Tip – Create a Digital Claims Folder: After every towing or roadside event, immediately photograph all documents and save them to a clearly labeled folder on your phone or cloud storage. Call your insurer from that folder so everything is at your fingertips during the call. A two-minute organizational step at the scene saves hours of hunting for paperwork later. |

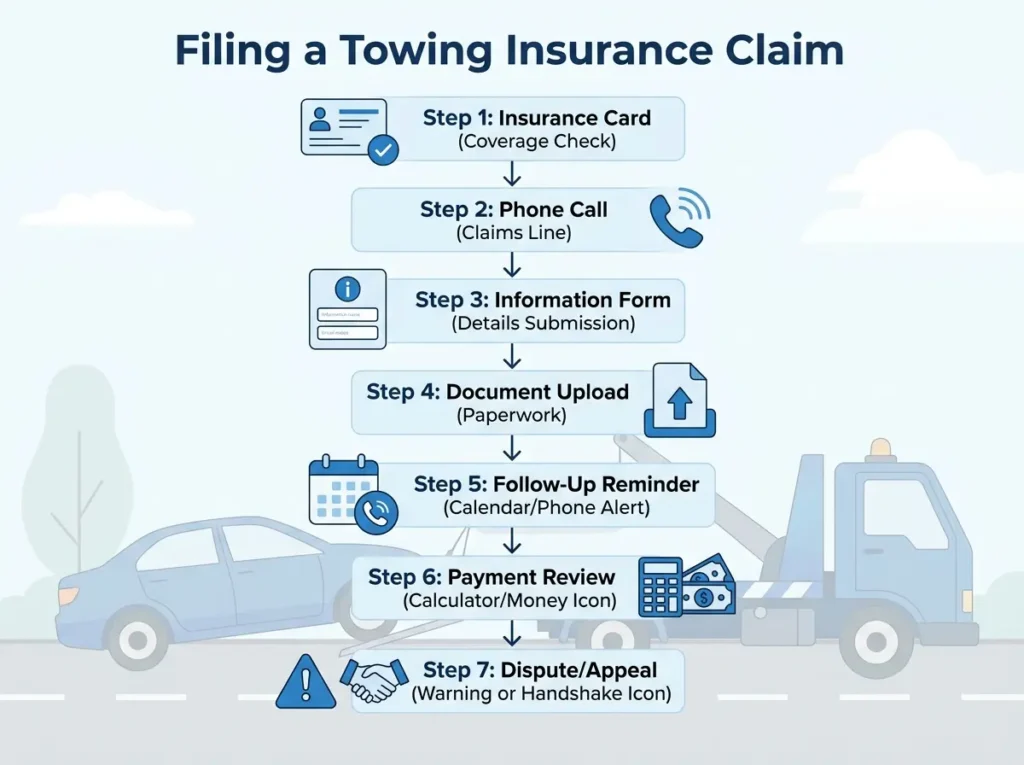

Step-by-Step: How to File a Towing Insurance Claim

Whether you paid out of pocket and are seeking reimbursement, or you are filing a towing claim as part of a broader accident claim, the following process applies across virtually all major insurance providers.

Step 1: Confirm Your Coverage Type

Check whether you have a roadside assistance add-on, collision coverage, comprehensive coverage, or all three. Knowing which coverage applies to your situation saves time on the call and ensures the claim is filed under the correct policy component.

Step 2: Call Your Insurer’s Claims Line

Contact your insurer’s dedicated claims number, not the general customer service line. Most insurers have a dedicated claims number on your insurance card and in your policy documents. For roadside reimbursement claims, many insurers also offer online or app-based submission.

Step 3: Provide Essential Information

Share your policy number, the date and location of the incident, a description of what happened, and the towing company’s information. The claims representative will open a claim file and give you a claim reference number. Write this down and keep it.

Step 4: Submit Your Documentation

Your insurer will tell you whether to email, fax, upload through their app, or mail your itemized invoice, receipt, and any supporting photos or police reports. Follow their preferred submission method and keep copies of everything you send.

Step 5: Follow Up on Your Claim

Follow up within 5 to 7 business days if you have not received a confirmation or update. Claims can get lost in queues, especially during high-volume winter periods when many Milwaukee drivers are filing simultaneously. A brief follow-up call citing your claim number keeps things moving.

Step 6: Review the Reimbursement Amount

When your reimbursement arrives, verify that the payment matches the coverage outlined in your policy. If the amount seems incorrect (less than your policy limit without explanation), request a written explanation from your claims adjuster and ask specifically whether any charges were excluded and why.

Step 7: Handle Denials or Underpayments

If your claim is denied or underpaid, request a formal denial letter explaining the specific reason. You have the right to appeal a denied claim, and a clear denial letter gives you the basis for that appeal. For complex or high-value claims, consulting a public adjuster or insurance attorney in Wisconsin may be worth the investment.

Need Towing in Milwaukee? We Make the Insurance Process Easy. MG Towing & Recovery – Itemized Invoices, Direct Insurance Billing, 24/7 Service

Filing a Towing Claim When the Other Driver Was at Fault

When your vehicle is towed as a result of an accident caused by another driver, the process is somewhat different from filing under your own policy. You have two options: file a third-party claim directly with the at-fault driver’s liability insurance, or file under your own collision coverage and let your insurer pursue the at-fault driver’s insurer through subrogation.

Third-Party Claim: Filing with the At-Fault Driver’s Insurer

A third-party towing claim means contacting the at-fault driver’s insurance company directly and filing a claim against their liability coverage. In this scenario, you are not using your own policy at all the at-fault driver’s insurer is responsible for your towing and related costs.

The advantage is that you do not pay a deductible. The disadvantage is that third-party claims can take longer to process, the at-fault driver’s insurer may dispute liability, and you have less control over the timeline.

During this waiting period, storage fees on your vehicle continue to accrue which is a real financial pressure that often leads drivers to accept lower settlements than they deserve simply to get the process moving.

Filing Through Your Own Collision Coverage (Subrogation)

Alternatively, you can file under your own collision coverage immediately, pay your deductible, and let your insurance company pursue the at-fault driver’s insurer for reimbursement through a legal process called subrogation. Once your insurer recovers the funds from the at-fault driver’s insurance, your deductible should be refunded to you.

This approach is often faster and less stressful than dealing directly with another driver’s insurer. Your own insurer is contractually obligated to process your claim; the at-fault driver’s insurer has no direct obligation to you and may be slower to respond.

| Milwaukee Practical Advice: In Milwaukee’s busy winter and pothole seasons, accident towing is common and insurers are processing high claim volumes. If you were not at fault, file under your own collision coverage immediately to stop storage fees from accumulating, and let your insurer handle the subrogation process. Do not let storage fees grow while waiting for the at-fault driver’s insurer to respond. |

Common Towing Insurance Claim Mistakes to Avoid

Many towing insurance claims that should be paid in full are delayed, reduced, or denied because of avoidable errors. Here are the most common tow truck insurance claim mistakes Milwaukee drivers make and how to avoid every one of them.

Mistake 1: Not Calling Your Insurer Before the Tow

Many roadside assistance policies require you to call your insurer’s dispatch center first so they can authorize the service and dispatch a preferred provider.

If you call an independent towing company directly without prior authorization, your insurer may deny reimbursement on the grounds that you did not follow the required process. Always check whether pre-authorization is required under your policy before the tow begins.

Mistake 2: Accepting a Lump-Sum Receipt Instead of an Itemized Invoice

A receipt that says simply “Towing Services – $200” gives your insurer nothing to work with. Always insist on an itemized invoice listing each charge individually. If a towing company refuses to provide an itemized invoice, that is a serious red flag about their business practices and a potential problem for your claim.

Mistake 3: Waiting Too Long to File

Insurance policies have filing deadlines. Missing them even by a few days can result in complete denial of an otherwise valid claim. File your towing reimbursement claim as soon as you have your documentation in hand, ideally within 24 to 48 hours of the incident. Do not set the paperwork aside and forget about it.

Mistake 4: Not Documenting the Vehicle’s Condition Before the Tow

Without before-tow photos, you have no evidence of your vehicle’s pre-tow condition. If additional damage occurs during towing and the towing company disputes responsibility, or if your insurer questions the extent of damage claimed, you have nothing to fall back on. Taking photos before the vehicle is loaded takes two minutes and protects you from potentially expensive disputes.

Mistake 5: Confusing Roadside Assistance Coverage with Collision Coverage

These two coverage types cover different situations and have different claims processes. Filing a breakdown tow under collision coverage when you have a roadside add-on or vice versa can lead to a delay or denial while the claim is rerouted internally.

Know which coverage applies to your specific situation before you call. When in doubt, describe the situation to your claims representative and let them direct you.

Mistake 6: Ignoring Storage Fees While Waiting for Claim Processing

Storage fees at towing yards accumulate every single day, and insurers typically only cover storage fees for a limited number of days often three to five.

If your vehicle sits at a tow yard for ten days while you wait for your claim to process, you may be responsible for seven or more days of storage fees out of pocket. Move your vehicle to a repair shop or other location as quickly as possible to minimize accruing storage costs.

Mistake 7: Not Appealing a Denied Claim

A denied towing insurance claim is not necessarily the final word. Insurers make errors, and claims are sometimes denied for technical reasons that can be corrected. If your claim is denied, request a formal written denial with the specific reason stated. Review the denial against your actual policy language, if the denial reason does not align with your policy terms, file a formal appeal.

Wisconsin drivers also have the right to file a complaint with the Wisconsin Office of the Commissioner of Insurance if they believe a denial is improper.

| Denied Claim? Know Your Rights: In Wisconsin, insurance companies must handle claims in good faith and within a reasonable timeframe. If you believe your towing claim was wrongfully denied or unreasonably delayed, you can file a complaint with the Wisconsin Office of the Commissioner of Insurance (OCI). Keeping detailed records of all communications with your insurer is essential if a dispute escalates. |

Towing Insurance Claim Cost Reimbursement: What to Realistically Expect

Understanding what your insurer will and will not reimburse and in what amounts prevents unpleasant surprises when the check or direct deposit arrives. Here is a realistic breakdown of tow truck claim cost reimbursement for common Milwaukee towing scenarios.

| Scenario | Typical Tow Cost | Likely Coverage | Out-of-Pocket Risk |

| Breakdown tow – roadside add-on | $75–$175 | Full cost to policy limit | Overage if tow exceeds limit |

| Accident tow – collision coverage | $100–$300 | Included in claim (deductible applies) | Deductible amount |

| At-fault driver’s insurer (3rd party) | $100–$300 | Full cost typically covered | Delays while liability disputed |

| Long-distance tow – roadside add-on | $300–$600+ | Up to mileage/dollar cap | Excess beyond cap |

| Storage fees – roadside add-on | $35–$75/day | Often 3–5 days only | Beyond covered days |

| Snow recovery – roadside add-on | $75–$250+ | Often covered if policy includes recovery | Varies – confirm in advance |

How to Maximize Your Towing Reimbursement?

- Know your per-incident towing limit before you call, if your limit is $100 and the tow costs $175, ask the towing company whether they will accept the insurance payment directly and waive or reduce the balance

- Use your insurer’s preferred or network tow providers when possible, in-network providers often have pre-negotiated rates that stay within policy limits

- Move your vehicle from the tow yard to a repair shop as quickly as possible to minimize storage fees beyond your covered days

- Keep every receipt, invoice, and communication related to the towing event even for charges that seem unlikely to be covered, submit them all and let the insurer determine coverage

- Ask your insurer specifically whether a flatbed tow, long-distance tow, or specialty vehicle tow is covered at the same rate as a standard tow or whether separate limits apply

Roadside Assistance Insurance Tips for Milwaukee Drivers

Being informed before an emergency happens is the single most valuable thing a Milwaukee driver can do regarding towing coverage. These practical tips help you get maximum value from whatever coverage you currently have and identify gaps worth addressing before winter.

Understanding Your Current Coverage

Review your current policy’s roadside assistance section today. Know your per-incident limit, your annual claim limit, and whether pre-authorization is required before calling a towing company.

Adding Roadside Assistance

Add roadside assistance to your policy if you do not have it. The annual cost of $36 to $180 is recovered in a single incident, and Milwaukee winters virtually guarantee you will need it eventually.

Emergency Preparedness

Save your insurer’s 24/7 roadside claims number in your phone as a contact, not buried in a glove box document you will not find at two in the morning during a Milwaukee winter breakdown.

AAA Membership Considerations

If you belong to AAA, carry your membership card and know which AAA tier you are on. Different tiers have different mileage limits that affect your out-of-pocket exposure on longer tows.

Credit Card Benefits

Check your credit cards for roadside assistance benefits. Some premium cards include towing coverage that duplicates your insurer’s roadside add-on, potentially doubling your available reimbursement channels.

Annual Coverage Review

After each winter, review whether your towing coverage limits are still adequate. If towing costs in Milwaukee have increased, your fixed-dollar limit may no longer cover a full local tow.

Choosing the Right Towing Company

When you choose a Milwaukee towing company, choose one that provides itemized invoices, accepts direct insurance billing, and has experience working with insurance claims. MG Transportation LLC handles insurance billing directly, simplifying the claim process for our customers.

Frequently Asked Questions: Towing Insurance Claims

Q. How long does a towing insurance claim typically take to process?

For straightforward roadside assistance reimbursement claims with complete documentation, many insurers process payment within five to fifteen business days of receiving all required documents.

Accident-related towing claims that are part of a broader collision claim may take longer particularly if liability is disputed or vehicle damage assessment is complex. Following up after seven business days if you have not received an update is reasonable and often accelerates the process.

Q. Will filing a towing insurance claim raise my premium?

Filing a claim under your roadside assistance add-on generally does not affect your premium in most states and with most major insurers roadside assistance is typically treated as a separate service benefit rather than an accident claim.

However, filing a collision or comprehensive claim (for accident towing) may affect your rates at renewal depending on your insurer’s policies and your claims history. If the towing cost is less than or close to your deductible, it may not be worth filing a collision claim at all, consult with your agent about the rate impact before deciding.

What if the towing company charges more than my insurance covers?

You are responsible for the difference between the towing company’s charge and your insurance policy’s coverage limit. To minimize this gap, always ask your insurer about in-network towing providers whose rates fall within policy limits, and ask the towing company whether they accept direct insurance payment and will waive or negotiate the balance.

Getting a written estimate before the tow begins also allows you to call your insurer and confirm coverage in advance if the estimated cost appears to exceed your limit.

Can I claim towing costs if I have only liability coverage?

Standard liability coverage does not cover towing costs for your own vehicle. Liability insurance pays for damage you cause to other people and property not your own vehicle’s recovery or transport costs.

To have towing covered, you need either a roadside assistance endorsement, collision coverage, comprehensive coverage, or a third-party membership like AAA. If you currently carry liability only and drive regularly in Milwaukee winters, adding a roadside assistance endorsement is strongly recommended.

Does my insurance cover towing for a flat tire or dead battery if I need to go to a shop?

Yes – if you have a roadside assistance endorsement, it typically covers towing to the nearest repair facility when a flat tire cannot be changed on-site or a battery issue requires the vehicle to be taken to a shop.

The coverage applies to the tow itself, not the repair. Some policies cover a tire change on-site as a roadside service first, and towing only if the on-site service cannot resolve the problem. Check your specific policy language for the exact conditions.

File Smart: Get Every Dollar You Are Owed

Filing an insurance claim for towing services is not complicated but it does require knowing your coverage, gathering the right documentation promptly, and avoiding the common mistakes that lead to delays and denials. Every Milwaukee driver who has ever paid a towing bill out of pocket and later discovered it could have been reimbursed knows how frustrating that is.

The practical takeaways from this guide are straightforward: know your towing coverage limits before an emergency, call your insurer as part of your immediate response rather than as an afterthought, always get an itemized invoice, document the scene thoroughly, and file without delay. These habits turn what could be a complicated reimbursement struggle into a smooth, routine transaction.

At MG Towing & Recovery, we make the insurance side of towing as simple as possible for Milwaukee drivers. We provide itemized invoices on every tow, offer direct insurance billing to major carriers, and our staff can help you understand what documentation you will need for your specific claim.

When you call us for towing or roadside assistance in Milwaukee, we are not just here to move your vehicle, we are here to make the entire experience as painless as possible, from the first call to the final reimbursement.